Your Money Matters. Stay Educated and Informed.

Our goal isn't just to manage your money, but to make sure you understand exactly where it is going. We are going to build this strategy around your specific comfort level, and want you to be informed on the decisions we are making.

Financial Planning

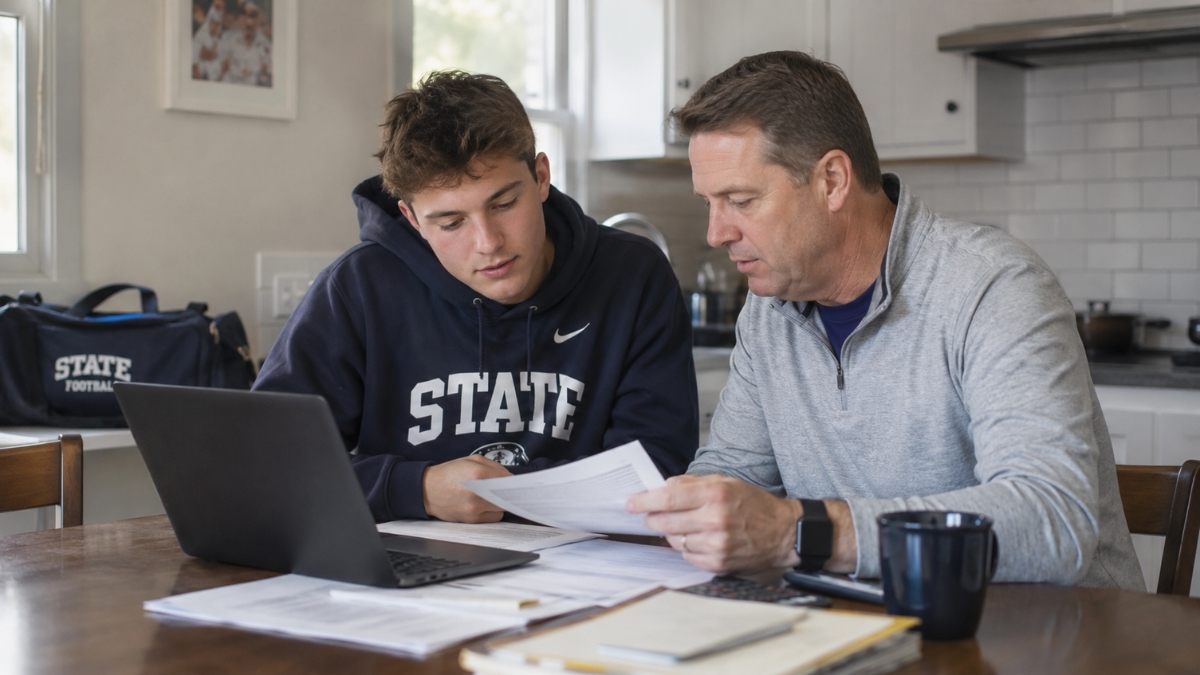

NIL Financial Planning Guide for College Athletes and Families

May 20, 2026

Name, image, and likeness (NIL) income has changed what it means to be a college athlete. For some athletes, NIL money may start as a few local appearances, a few social media posts, or a local sponsorship. For others, it

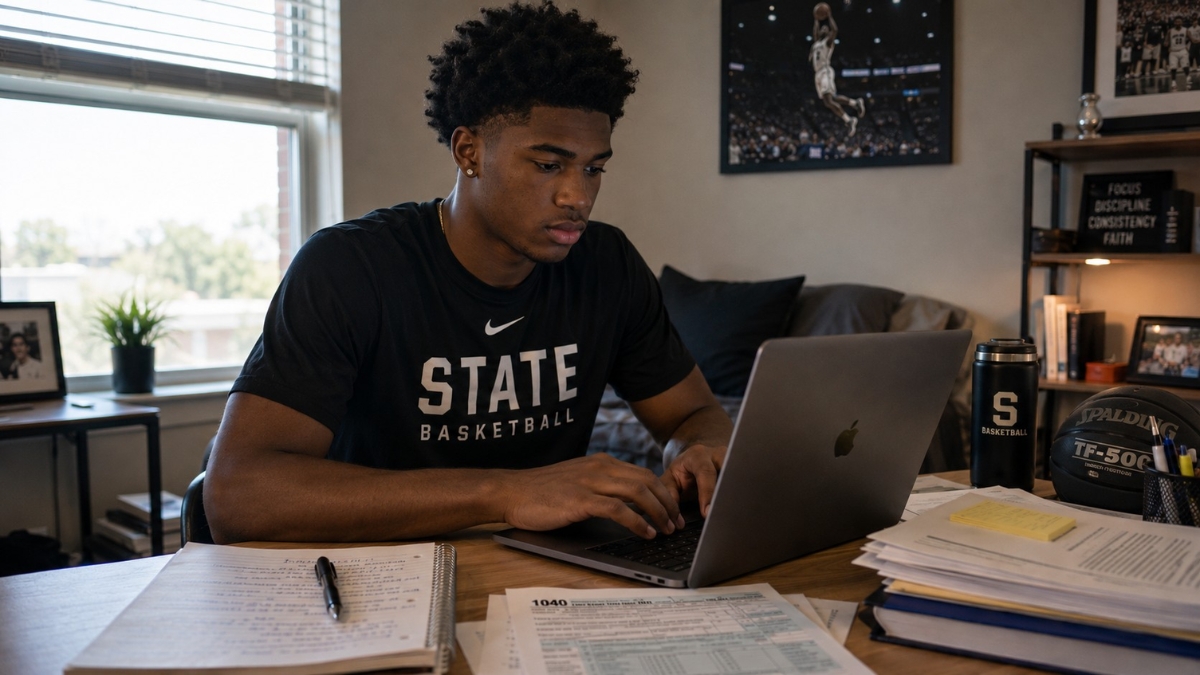

What Taxes Do College Athletes Pay on NIL Income?

April 8, 2026

NIL income can be exciting for college athletes and families, but it also introduces a tax responsibility many students have never dealt with before. Unlike a traditional paycheck, many NIL payments do not have taxes withheld before the money is

Quarterly Taxes for NIL Income

March 25, 2026

Many college athletes earning NIL income are surprised to learn that taxes may need to be paid during the year, not just when a tax return is filed. This is where quarterly estimated taxes come in. Quarterly taxes are not

Investing

Tax Loss Harvesting Explained: What Investors Need to Know

May 2, 2026

Tax loss harvesting often gets attention because it sounds like a simple way to turn market declines into something useful. And in certain situations, it can do exactly that. But in practice, it tends to be most effective when it

Why Investors Underperform Their Own Portfolios

April 16, 2026

Investors often assume underperformance comes from owning the wrong funds, the wrong stocks, or the wrong managers. Sometimes that is true. More often, the bigger issue is behavior. A portfolio can be well constructed on paper and still produce disappointing

Concentrated Stock Risk: Why It Deserves Extra Attention

April 10, 2026

Concentrated stock risk often builds quietly. A position may start as a success story, an equity compensation award, or a legacy holding that has appreciated over time. Eventually it becomes large enough that one company has an outsized influence on

Market Insights

U.S. and Iran Conflict: What War Headlines Mean for Markets and Investors

March 12, 2026

Over the past two weeks, major headlines have emerged from the Middle East following U.S. military strikes against Iran. Whenever events like this unfold, investors naturally begin asking difficult questions. Is this the beginning of a larger conflict? Will markets

2026 Market & Economic Outlook: Becoming Hopeful Realists in an Unstable World

January 17, 2026

After several years of economic whiplash, investors enter 2026 with a familiar tension: optimism fueled by strong market returns and technological innovation, alongside persistent concerns about inflation, interest rates, valuations, and economic inequality. At Navalign, we believe this is not

First Quarter 2026: AI Growth, Iran War, and Volatility

April 7, 2026

During our outlook at the start of the year, we highlighted two key themes: So far, both have played out. The economy has remained resilient, supported by steady consumer activity and significant capital flowing into AI infrastructure. At the same time, markets have faced